Perceived Security and Trust as Mechanisms of P2P Adoption Technology: Evidence from Pre-Adopters Using PLS-SEM Approach

Article Sidebar

Main Article Content

Abstract

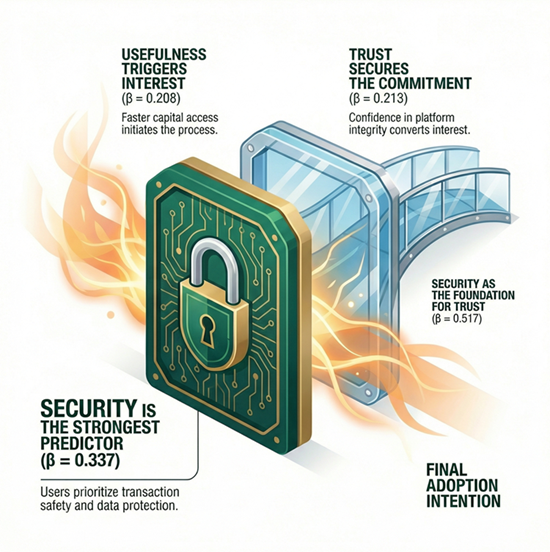

Peer-to-peer (P2P) lending can expand working-capital access for micro-entrepreneurs, yet borrowing via digital platforms heightens perceived vulnerability due to sensitive data disclosure and binding repayment obligations. This study examines how perceived security and trust shape adoption intention in a high-stakes fintech context by extending the Technology Acceptance Model (TAM) and testing whether security and trust transmit the effect of perceived usefulness to intention. Using an explanatory cross-sectional design, we collected offline-administered survey data from 204 Indonesian micro-entrepreneurs who had not previously adopted P2P lending to capture pre-adopter perceptions better and reduce digital-selection bias. The model was estimated using PLS-SEM 3. The results indicate that all hypothesized relationships are positive and statistically significant. Perceived usefulness significantly enhances perceived security (β = 0.562) and trust (β = 0.259), while perceived security exerts a strong positive effect on trust (β = 0.517). Intention to use P2P lending is directly influenced by perceived security (β = 0.337), trust (β = 0.213), and perceived usefulness (β = 0.208). Mediation analysis confirms that perceived security (β = 0.189) and trust (β = 0.055) partially mediate the effect of perceived usefulness on intention to use. The model explains 42.4% of the variance in intention to use (R-squared = 0.424) and demonstrates adequate predictive relevance (Q-squared = 0.263). Overall, perceived security emerges as the most influential determinant of adoption intention, underscoring the importance of security-by-design features, transparent governance, and robust consumer-protection frameworks in fostering trust and accelerating P2P lending adoption among micro-entrepreneurs.

Downloads

Article Details

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

Authors who publish with this journal agree to the following terms:

- Copyright of the published article belongs to the authors and grant the journal right of first publication with the work simultaneously licensed under a Creative Commons Attribution-ShareAlike 4.0 (CC BY SA) International License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this journal.

- Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the journal's published version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial publication in this journal.

- Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See the Effect of Open Access).

References

[1] P. Gomber, R. J. Kauffman, C. Parker, and B. W. Weber, “On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services,” J. Manag. Inf. Syst., vol. 35, no. 1, pp. 220–265, 2018, https://doi.org/10.1080/07421222.2018.1440766

[2] A. Thakor, “Corrigendum to: Fintech and Banking: What Do We Know?,” J. Financ. Intermediation, vol. 43, p. 100833, 2020, https://doi.org/10.1016/j.jfi.2020.100858

[3] C. F. Breidbach, B. W. Keating, and C. Lim, “Fintech: research directions to explore the digital transformation of financial service systems,” J. Serv. Theory Pract., vol. 30, no. 1, pp. 79–102, 2020, https://doi.org/10.1108/JSTP-08-2018-0185

[4] R. Iyer, A. I. Khwaja, E. F. P. Luttmer, and K. Shue, “Screening peers softly: Inferring the quality of small borrowers,” Manage. Sci., vol. 62, no. 6, pp. 1554–1577, 2016, https://doi.org/10.1287/mnsc.2015.2181

[5] A. Morse, “Peer-to-Peer Crowdfunding: Information and the Potential for Disruption in Consumer Lending,” Annu. Rev. Financ. Econ., vol. 7, no. 1, pp. 463–482, 2015, https://doi.org/10.1146/annurev-financial-111914-041939

[6] Boeddu et al., “Consumer risks in fintech - new manifestations of consumer risks and emerging regulatory approaches : Policy research paper,” World Bank Group, 2021. http://documents.worldbank.org/curated/en/515771621921739154

[7] D. Burton, “Digital Debt Collection and Ecologies of Consumer Overindebtedness,” Econ. Geogr., vol. 96, no. 3, pp. 244–265, 2020, https://doi.org/10.1080/00130095.2020.1762486

[8] OECD, “Financial Consumer Protection Policy Approaches in the Digital Age: Protecting consumers’ assets, data and privacy.” OECD Publishing, Paris, 2020. https://doi.org/10.1787/3f205e60-en

[9] M. Bazarbash and K. Beaton, “Filling the Gap: Digital Credit and Financial Inclusion,” IMF Work. Pap., vol. 2020, no. 150, p. 30, 2020, [Online]. Available: https://www.elibrary.imf.org/view/journals/001/2020/150/article-A001-en.xml

[10] J. Frost, L. Gambacorta, Y. Huang, H. Song Shin, and P. Zbinden, “BigTech and the changing structure of financial intermediation,” Econ. Policy, vol. 34, no. 100, pp. 761–799, 2019, https://doi.org/10.1093/EPOLIC/EIAA003

[11] D. W. Arner, J. Barberis, and R. P. Buckley, “FinTech, regTech, and the reconceptualization of financial regulation,” Northwest. J. Int. Law Bus., vol. 37, no. 3, pp. 373–415, 2017.

[12] S. T. Omarova, “Fintech and the limits of financial regulation: A systemic perspective,” in Routledge Handbook of Financial Technology and Law, Routledge, 2021, pp. 44–61. https://doi.org/10.4324/9780429325670-3

[13] M. S. Featherman and P. A. Pavlou, “Predicting e-services adoption: A perceived risk facets perspective,” Int. J. Hum. Comput. Stud., vol. 59, no. 4, pp. 451–474, 2003, https://doi.org/10.1016/S1071-5819(03)00111-3

[14] T. Roh, Y. S. Yang, S. Xiao, and B. Il Park, “What makes consumers trust and adopt fintech? An empirical investigation in China,” Electron. Commer. Res., vol. 24, no. 1, pp. 3–35, 2024, https://doi.org/10.1007/s10660-021-09527-3

[15] D. J. Kim, D. L. Ferrin, and H. R. Rao, “A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents,” Decis. Support Syst., vol. 44, no. 2, pp. 544–564, 2008, https://doi.org/10.1016/j.dss.2007.07.001

[16] I. Ajzen, “The Theory of planned behavior,” Organ. Behav. Hum. Decis. Process., 1991.

[17] M. Fishbein and I. Ajzen, Belief, attitude, intention and behavior: An introduction to theory and research. 1975.

[18] F. D. Davis, “Perceived usefulness, perceived ease of use, and user acceptance of information technology,” MIS Q. Manag. Inf. Syst., vol. 13, no. 3, pp. 319–339, 1989, https://doi.org/10.2307/249008

[19] M. T. Dishaw and D. M. Strong, “Extending the technology acceptance model with task-technology fit constructs,” Inf. Manag., vol. 36, no. 1, pp. 9–21, 1999, https://doi.org/10.1016/S0378-7206(98)00101-3

[20] B. Wu and X. Chen, “Continuance intention to use MOOCs: Integrating the technology acceptance model (TAM) and task technology fit (TTF) model,” Comput. Human Behav., vol. 67, pp. 221–232, 2017, https://doi.org/10.1016/j.chb.2016.10.028

[21] D. H. McKnight, V. Choudhury, and C. Kacmar, “Developing and validating trust measures for e-commerce: An integrative typology,” Inf. Syst. Res., vol. 13, no. 3, pp. 334–359, 2002, https://doi.org/10.1287/isre.13.3.334.81

[22] H. Stewart and J. Jürjens, “Data security and consumer trust in FinTech innovation in Germany,” Inf. Comput. Secur., vol. 26, no. 1, pp. 109–128, 2018, https://doi.org/10.1108/ICS-06-2017-0039

[23] D. Okat, M. Paaso, and V. Pursiainen, “Trust in Traditional Finance and Consumer Fintech Adoption,” Rev. Corp. Financ. Stud., vol. 14, no. 2, pp. 408–438, 2025, https://doi.org/10.1093/rcfs/cfae011

[24] J. Bethlehem, “Selection bias in web surveys,” Int. Stat. Rev., vol. 78, no. 2, pp. 161–188, 2010, https://doi.org/10.1111/j.1751-5823.2010.00112.x

[25] M. P. Couper, “Web surveys: A review of issues and approaches,” Public Opin. Q., vol. 64, no. 4, pp. 464–494, 2000, https://doi.org/10.1086/318641

[26] I. D. Wijaya, E. S. Astuti, E. Yulianto, and Y. Abdillah, “Examining the impact of perceived usefulness on micro-entrepreneurs’ intentions to use Fintech peer to peer lending applications with perceived security as a mediating factor,” Multidiscip. Sci. J., vol. 7, no. 10, p. 2025483, 2025, https://doi.org/10.31893/multiscience.2025483

[27] A. Milazzo and M. Goldstein, “Governance and women’s economic and political participation: Power inequalities, formal constraints and norms,” World Bank Res. Obs., vol. 34, no. 1, pp. 34–64, 2019, https://doi.org/10.1093/wbro/lky006

[28] P. Gomber, J. A. Koch, and M. Siering, “Digital Finance and FinTech: current research and future research directions,” J. Bus. Econ., vol. 87, no. 5, pp. 537–580, 2017, https://doi.org/10.1007/s11573-017-0852-x

[29] M. Bazarbash, FinTech in Financial Inclusion: Machine Learning Applications in Assessing Credit Risk, vol. 2019, no. 109. International Monetary Fund, 2019. https://doi.org/10.5089/9781498314428.001

[30] T. Dahlberg, J. Guo, and J. Ondrus, “A critical review of mobile payment research,” Electron. Commer. Res. Appl., vol. 14, no. 5, pp. 265–284, 2015, https://doi.org/10.1016/j.elerap.2015.07.006

[31] OECD, “G20/OECD Report on Lessons Learnt and Effective Approaches to Protect Consumers and Support Financial Inclusion in the Context of COVID-19,” 2021.

[32] B. Chang, S. Y. Chen, Y. C. Tsai, and M. L. Lai, “The effects of task activities and gaming scales on eye reading and visual search performance,” Comput. Human Behav., vol. 66, pp. 16–25, 2017, https://doi.org/10.1016/j.chb.2016.09.013

[33] D. A. Zetzsche, D. W. Arner, R. P. Buckley, and R. H. Weber, “The Future of Data-Driven Finance and RegTech: Lessons from EU Big Bang II,” SSRN Electron. J., vol. 25, p. 245, 2019, https://doi.org/10.2139/ssrn.3359399

[34] P. A. Pavlou, “Consumer acceptance of electronic commerce: Integrating trust and risk with the technology acceptance model,” Int. J. Electron. Commer., vol. 7, no. 3, pp. 101–134, 2003, https://doi.org/10.1080/10864415.2003.11044275

[35] D. Gefen, I. Benbasat, and P. A. Pavlou, “A research agenda for trust in online environments,” J. Manag. Inf. Syst., vol. 24, no. 4, pp. 275–286, 2008, https://doi.org/10.2753/MIS0742-1222240411

[36] V. Venkatesh, J. Y. L. Thong, and X. Xu, “Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology,” MIS Q. Manag. Inf. Syst., vol. 36, no. 1, pp. 157–178, 2012, https://doi.org/10.2307/41410412

[37] I. Ajzen, “Perceived behavioral control, self-efficacy, locus of control, and the theory of planned behavior,” J. Appl. Soc. Psychol., vol. 32, no. 4, pp. 665–683, 2002, https://doi.org/10.1111/j.1559-1816.2002.tb00236.x

[38] C. J. Armitage and M. Conner, “Efficacy of the theory of planned behaviour: A meta-analytic review,” Br. J. Soc. Psychol., vol. 40, no. 4, pp. 471–499, 2001, https://doi.org/10.1348/014466601164939

[39] I. Ajzen, “The theory of planned behavior: Frequently asked questions,” Hum. Behav. Emerg. Technol., vol. 2, no. 4, pp. 314–324, 2020.

[40] I. Ajzen and M. Fishbein, Understanding attitudes and predictiing social behavior. Englewood Cliffs: Prentice-hall, 1980.

[41] P. Sheeran, “Intention—Behavior Relations: A Conceptual and Empirical Review,” Eur. Rev. Soc. Psychol., vol. 12, no. 1, pp. 1–36, 2002, https://doi.org/10.1080/14792772143000003

[42] U. R. Orth, S. Hoffmann, and K. Nickel, “Moral decoupling feels good and makes buying counterfeits easy,” J. Bus. Res., vol. 98, pp. 117–125, 2019, https://doi.org/10.1016/j.jbusres.2019.01.001

[43] V. Venkatesh, M. G. Morris, G. B. Davis, and F. D. Davis, “User acceptance of information technology: Toward a unified view,” MIS Q. Manag. Inf. Syst., vol. 27, no. 3, pp. 425–478, 2003, https://doi.org/10.2307/30036540

[44] P. Sheeran and T. L. Webb, “The intention–behavior gap,” Soc. Personal. Psychol. Compass, vol. 10, no. 9, pp. 503–518, 2016.

[45] F. D. Davis, R. P. Bagozzi, and P. R. Warshaw, “User Acceptance of Computer Technology: A Comparison of Two Theoretical Models,” Manage. Sci., vol. 35, no. 8, pp. 982–1003, 1989, https://doi.org/10.1287/mnsc.35.8.982

[46] D. Chawla and H. Joshi, “Consumer attitude and intention to adopt mobile wallet in India – An empirical study,” Int. J. Bank Mark., vol. 37, no. 7, pp. 1590–1618, 2019, https://doi.org/10.1108/IJBM-09-2018-0256

[47] M. Najib and F. Fahma, “Investigating the adoption of digital payment system through an extended technology acceptance model: An insight from the Indonesian small and medium enterprises,” Int. J. Adv. Sci. Eng. Inf. Technol., vol. 10, no. 4, pp. 1702–1708, 2020, https://doi.org/10.18517/ijaseit.10.4.11616

[48] A. A. Alalwan, Y. K. Dwivedi, N. P. P. Rana, and M. D. Williams, “Consumer adoption of mobile banking in Jordan: Examining the role of usefulness, ease of use, perceived risk and self-efficacy,” J. Enterp. Inf. Manag., vol. 29, no. 1, pp. 118–139, 2016, https://doi.org/10.1108/JEIM-04-2015-0035

[49] A. Daragmeh, C. Lentner, and J. Sági, “FinTech payments in the era of COVID-19: Factors influencing behavioral intentions of ‘Generation X’ in Hungary to use mobile payment,” J. Behav. Exp. Financ., vol. 32, p. 100574, 2021, https://doi.org/10.1016/j.jbef.2021.100574

[50] A. T. To and T. H. M. Trinh, “Understanding behavioral intention to use mobile wallets in vietnam: Extending the TAM model with trust and enjoyment,” Cogent Bus. Manag., vol. 8, no. 1, p. 1891661, 2021, https://doi.org/10.1080/23311975.2021.1891661

[51] D. Gefen, E. Karahanna, and D. W. Straub, “Trust and tam in online shopping: AN integrated model,” MIS Q. Manag. Inf. Syst., vol. 27, no. 1, pp. 51–90, 2003, https://doi.org/10.2307/30036519

[52] N. Singh, N. Sinha, and F. J. Liébana-Cabanillas, “Determining factors in the adoption and recommendation of mobile wallet services in India: Analysis of the effect of innovativeness, stress to use and social influence,” Int. J. Inf. Manage., vol. 50, pp. 191–205, 2020, https://doi.org/10.1016/j.ijinfomgt.2019.05.022

[53] A. Kumar, A. Adlakaha, and K. Mukherjee, “The effect of perceived security and grievance redressal on continuance intention to use M-wallets in a developing country,” Int. J. Bank Mark., vol. 36, no. 7, pp. 1170–1189, 2018, https://doi.org/10.1108/IJBM-04-2017-0077

[54] I. Arpaci, Y. Yardimci Cetin, and O. Turetken, “Impact of Perceived Security on Organizational Adoption of Smartphones,” Cyberpsychology, Behav. Soc. Netw., vol. 18, no. 10, pp. 602–608, 2015, https://doi.org/10.1089/cyber.2015.0243

[55] E. Oney, G. O. Guven, and W. H. Rizvi, “The determinants of electronic payment systems usage from consumers’ perspective,” Econ. Res. istraživanja, vol. 30, no. 1, pp. 394–415, 2017. https://doi.org/10.1080/1331677X.2017.1305791

[56] B. Setiawan, D. P. Nugraha, A. Irawan, R. J. Nathan, and Z. Zoltan, “User innovativeness and fintech adoption in indonesia,” J. Open Innov. Technol. Mark. Complex., vol. 7, no. 3, p. 188, 2021, https://doi.org/10.3390/joitmc7030188

[57] J. Wu, L. Liu, and L. Huang, “Consumer acceptance of mobile payment across time Antecedents and moderating role of diffusion stages,” Ind. Manag. Data Syst., vol. 117, no. 8, pp. 1761–1776, 2017, https://doi.org/10.1108/IMDS-08-2016-0312

[58] N. Singh and N. Sinha, “How perceived trust mediates merchant’s intention to use a mobile wallet technology,” J. Retail. Consum. Serv., vol. 52, p. 101894, 2020, https://doi.org/10.1016/j.jretconser.2019.101894

[59] M. A. Almaiah et al., “Investigating the effect of perceived security, perceived trust, and information quality on mobile payment usage through near-field communication (NFC) in Saudi Arabia,” Electronics, vol. 11, no. 23, p. 3926, 2022. https://doi.org/10.3390/electronics11233926

[60] G. Albort-Morant, C. Sanchís-Pedregosa, and J. R. Paredes Paredes, “Online banking adoption in Spanish cities and towns. Finding differences through TAM application,” Econ. Res. istraživanja, vol. 35, no. 1, pp. 854–872, 2022. https://doi.org/10.1080/1331677X.2021.1945477

[61] M. K. Al Nawayseh, “Fintech in COVID-19 and beyond: What factors are affecting customers’ choice of fintech applications?,” J. Open Innov. Technol. Mark. Complex., vol. 6, no. 4, p. 153, 2020. https://doi.org/10.3390/joitmc6040153

[62] D. P. Nugraha, B. Setiawan, R. J. Nathan, and M. Fekete-Farkas, “FinTech adoption drivers for innovation for SMEs in Indonesia,” J. Open Innov. Technol. Mark. Complex., vol. 8, no. 4, p. 208, 2022. https://doi.org/10.3390/joitmc8040208

[63] D. Gefen, “TAM or just plain habit: A look at experienced online shoppers,” J. End User Comput., vol. 15, no. 3, pp. 1–13, 2003, https://doi.org/10.4018/joeuc.2003070101

[64] V. Venkatesh and F. D. Davis, “Theoretical extension of the Technology Acceptance Model: Four longitudinal field studies,” Manage. Sci., vol. 46, no. 2, pp. 186–204, 2000, https://doi.org/10.1287/mnsc.46.2.186.11926

[65] V. Venkatesh and H. Bala, “Technology acceptance model 3 and a research agenda on interventions,” Decis. Sci., vol. 39, no. 2, pp. 273–315, 2008, https://doi.org/10.1111/j.1540-5915.2008.00192.x

[66] W. D. Salisbury, R. A. Pearson, A. W. Pearson, and D. W. Miller, “Perceived security and World Wide Web purchase intention,” Ind. Manag. Data Syst., vol. 101, no. 4, pp. 165–177, 2001, https://doi.org/10.1108/02635570110390071

[67] C. Flavián and M. Guinalíu, “Consumer trust, perceived security and privacy policy,” Ind. Manag. Data Syst., vol. 106, no. 5, pp. 601–620, 2006, https://doi.org/10.1108/02635570610666403

[68] C. Kim, M. Mirusmonov, and I. Lee, “An empirical examination of factors influencing the intention to use mobile payment,” Comput. Human Behav., vol. 26, no. 3, pp. 310–322, 2010, https://doi.org/10.1016/j.chb.2009.10.013

[69] A. Bhattacherjee, “Understanding information systems continuance: An expectation-confirmation model,” MIS Q. Manag. Inf. Syst., vol. 25, no. 3, pp. 351–370, 2001, https://doi.org/10.2307/3250921

[70] M. Sarstedt, C. M. Ringle, and J. F. Hair, Partial Least Squares Structural Equation Modeling. Asheboro, USA: Statistical Publishing Associates, 2021. https://doi.org/10.1007/978-3-319-57413-4_15

[71] J. F. Hair, J. J. Risher, M. Sarstedt, and C. M. Ringle, “When to use and how to report the results of PLS-SEM,” Eur. Bus. Rev., vol. 31, no. 1, pp. 2–24, 2019, https://doi.org/10.1108/EBR-11-2018-0203

[72] M. Sarstedt, C. M. Ringle, J. H. Cheah, H. Ting, O. I. Moisescu, and L. Radomir, “Structural model robustness checks in PLS-SEM,” Tour. Econ., vol. 26, no. 4, pp. 531–554, 2020, https://doi.org/10.1177/1354816618823921

[73] C. M. Ringle, M. Sarstedt, R. Mitchell, and S. P. Gudergan, “Partial least squares structural equation modeling in HRM research,” Int. J. Hum. Resour. Manag., vol. 31, no. 12, pp. 1617–1643, 2020, https://doi.org/10.1080/09585192.2017.1416655

[74] J. F. Hair, C. M. Ringle, and M. Sarstedt, “PLS-SEM: Indeed a silver bullet,” J. Mark. Theory Pract., vol. 19, no. 2, pp. 139–152, 2011, https://doi.org/10.2753/MTP1069-6679190202

[75] J. Henseler, C. M. Ringle, and M. Sarstedt, “A new criterion for assessing discriminant validity in variance-based structural equation modeling,” J. Acad. Mark. Sci., vol. 43, no. 1, pp. 115–135, 2015, https://doi.org/10.1007/s11747-014-0403-8

[76] J. F. Hair Jr., L. M. Matthews, R. L. Matthews, and M. Sarstedt, “PLS-SEM or CB-SEM: updated guidelines on which method to use,” Int. J. Multivar. Data Anal., vol. 1, no. 2, p. 107, 2017, https://doi.org/10.1504/ijmda.2017.10008574

[77] J. D. Hundleby and J. Nunnally, Psychometric Theory, vol. 5, no. 3. New York, United States: McGraw-Hill Education, 1968. https://doi.org/10.2307/1161962

[78] R. P. Bagozzi and Y. Yi, “Specification, evaluation, and interpretation of structural equation models,” J. Acad. Mark. Sci., vol. 40, no. 1, pp. 8–34, 2012, https://doi.org/10.1007/s11747-011-0278-x

[79] M. Sarstedt, C. M. Ringle, and J. F. Hair, “Partial Least Squares Structural Equation Modeling,” Handbook of Market Research. Springer Nature, pp. 587–632, 2021. https://doi.org/10.1007/978-3-319-57413-4_15

[80] C. M. Voorhees, M. K. Brady, R. Calantone, and E. Ramirez, “Discriminant validity testing in marketing: an analysis, causes for concern, and proposed remedies,” J. Acad. Mark. Sci., vol. 44, no. 1, pp. 119–134, 2016, https://doi.org/10.1007/s11747-015-0455-4

[81] J. F. Hair, G. T. M. Hult, C. M. Ringle, M. Sarstedt, N. P. Danks, and S. Ray, “Evaluation of Reflective Measurement Models,” in Partial least squares structural equation modeling (PLS-SEM) using R: A workbook, Springer International Publishing Cham, 2021, pp. 75–90. https://doi.org/10.1007/978-3-030-80519-7_4

[82] W. W. Chin, “The partial least squares approach to structural equation modeling,” in Modern methods for business research, 1st ed., New York, United States: Psychology Press, 1998.

[83] J. F. Hair, M. Sarstedt, C. M. Ringle, and J. A. Mena, “An assessment of the use of partial least squares structural equation modeling in marketing research,” J. Acad. Mark. Sci., vol. 40, no. 3, pp. 414–433, 2012, https://doi.org/10.1007/s11747-011-0261-6

[84] J. F. Hair, W. C. Black, B. J. Babin, R. E. Anderson, and R. L. Tatham, Multivariate Data Analysis, 8th ed. Edinburgh Gate, Harlow: Pearson Education Limited, 2019.

[85] M. Stone, “Cross-Validatory Choice and Assessment of Statistical Predictions,” J. R. Stat. Soc. Ser. B Stat. Methodol., vol. 38, no. 1, pp. 102–102, 1976, https://doi.org/10.1111/j.2517-6161.1976.tb01573.x

[86] S. Geisser, “The predictive sample reuse method with applications,” J. Am. Stat. Assoc., vol. 70, no. 350, pp. 320–328, 1975, https://doi.org/10.1080/01621459.1975.10479865

[87] F. Belanger, J. S. Hiller, and W. J. Smith, “Trustworthiness in electronic commerce: The role of privacy, security, and site attributes,” J. Strateg. Inf. Syst., vol. 11, no. 3–4, pp. 245–270, 2002, https://doi.org/10.1016/S0963-8687(02)00018-5

[88] B. Suh and I. Han, “The impact of customer trust and perception of security control on the acceptance of electronic commerce,” Int. J. Electron. Commer., vol. 7, no. 3, pp. 135–161, 2003, https://doi.org/10.1080/10864415.2003.11044270

[89] D. Gefen, E. Karahanna, and D. W. Straub, “Inexperience and experience with online stores: The importance of TAM and trust,” IEEE Trans. Eng. Manag., vol. 50, no. 3, pp. 307–321, 2003, https://doi.org/10.1109/TEM.2003.817277

[90] H. S. Ryu, “Understanding benefit and risk framework of Fintech adoption: Comparison of early adopters and late adopters,” Proc. Annu. Hawaii Int. Conf. Syst. Sci., vol. 2018-Janua, pp. 3864–3873, 2018, https://doi.org/10.24251/hicss.2018.486

[91] D. Chen, F. Lai, and Z. Lin, “A trust model for online peer-to-peer lending: a lender’s perspective,” Inf. Technol. Manag., vol. 15, no. 4, pp. 239–254, 2014, https://doi.org/10.1007/s10799-014-0187-z

[92] R. Sunardi, H. Hamidah, A. Dharmawan BUCHDADI, and D. Purwana, “Factors Determining Adoption of Fintech Peer-to-Peer Lending Platform: An Empirical Study in Indonesia*,” J. Asian Financ., vol. 9, no. 1, pp. 43–0051, 2022, https://doi.org/10.13106/jafeb.2022.vol9.no1.0043

[93] G. A. Putri, A. K. Widagdo, and D. Setiawan, “Analysis of financial technology acceptance of peer-to-peer lending (P2P lending) using extended technology acceptance model (TAM),” J. Open Innov. Technol. Mark. Complex., vol. 9, no. 1, p. 100027, 2023, https://doi.org/10.1016/j.joitmc.2023.100027

[94] S. Candra, F. Nuruttarwiyah, and I. H. Hapsari, “Revisited the Technology Acceptance Model with E-Trust for Peer-to-Peer Lending in Indonesia (Perspective from Fintech Users),” Int. J. Technol., vol. 11, no. 4, pp. 710–721, 2020, https://doi.org/10.14716/ijtech.v11i4.4032

[95] T. Oliveira, M. Thomas, G. Baptista, and F. Campos, “Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology,” Comput. Human Behav., vol. 61, pp. 404–414, 2016, https://doi.org/10.1016/j.chb.2016.03.030

[96] G. Migliore, R. Wagner, F. S. Cechella, and F. Liébana-Cabanillas, “Antecedents to the Adoption of Mobile Payment in China and Italy: an Integration of UTAUT2 and Innovation Resistance Theory,” Inf. Syst. Front., vol. 24, no. 6, pp. 2099–2122, 2022, https://doi.org/10.1007/s10796-021-10237-2

[97] E. L. Slade, Y. K. Dwivedi, N. C. Piercy, and M. D. Williams, “Modeling Consumers’ Adoption Intentions of Remote Mobile Payments in the United Kingdom: Extending UTAUT with Innovativeness, Risk, and Trust,” Psychol. Mark., vol. 32, no. 8, pp. 860–873, 2015, https://doi.org/10.1002/mar.20823

[98] J. H. Jung, E. Kwon, and D. H. Kim, “Mobile payment service usage: U.S. consumers’ motivations and intentions,” Comput. Hum. Behav. Reports, vol. 1, p. 100008, 2020, https://doi.org/10.1016/j.chbr.2020.100008

[99] A. A. Bailey, I. Pentina, A. S. Mishra, and M. S. Ben Mimoun, “Exploring factors influencing US millennial consumers’ use of tap-and-go payment technology,” Int. Rev. Retail. Distrib. Consum. Res., vol. 30, no. 2, pp. 143–163, 2020, https://doi.org/10.1080/09593969.2019.1667854

[100] G. Cornelli, J. Frost, L. Gambacorta, and J. Jagtiani, “The impact of fintech lending on credit access for U.S. small businesses,” J. Financ. Stab., vol. 73, p. 101290, 2024, https://doi.org/10.1016/j.jfs.2024.101290

[101] C. Van Slyke, F. Belanger, and C. L. Comunale, “Factors Influencing the Adoption of Web-Based Shopping: The Impact of Trust,” Data Base Adv. Inf. Syst., vol. 35, no. 2, pp. 32–49, 2004, https://doi.org/10.1145/1007965.1007969

[102] M. Kim and M. Duvendack, “Fintech for the poor? Regulating the Kenyan digital credit market and its impact on borrowers,” Dev. Stud. Res., vol. 12, no. 1, p. 2547852, 2025, https://doi.org/10.1080/21665095.2025.2547852